1. Trends and Market Sentiment

The past two years have seen the creator economy surge in size and influence, driven by an explosion in both the number of creators and the ways they monetize content. Global Growth – Estimates valued the creator economy at around $250 billion in 2023, with projections of nearly $480 billion by 2027. The count of people identifying as content creators has skyrocketed – from roughly 50 million in 2021 to over 200 million creators worldwide in 2023 (including ~45 million “professional” full-time creators). This 314% increase in two years reflects how accessible content creation has become and how many are trying to turn their passion into a livelihood. A large share are “amateur” creators earning income on the side, but millions are pursuing content creation as a full-time career.

Earnings and Monetization Trends – A small top tier of creators earn exceptional incomes, but most operate at modest scales. Surveys indicate the majority of interviewed creators earn in the $50K–$100K per year range, while only about 4.8% of creators with 5M+ followers make over $1M annually. In fact, one analysis found 97.5% of YouTubers don’t earn enough to hit the U.S. poverty line from the platform alone, underscoring that the creator economy’s wealth is concentrated at the top. Still, overall creator earnings are climbing: on Patreon (a membership platform) annual payouts to creators jumped from $2.8 billion in 2022 to about $4.1 billion in 2023, and OnlyFans (an adult-focused platform) paid out $5.3 billion to creators in 2023, up 19% from the prior year. Creators are increasingly diversifying how they earn: beyond ad revenue and sponsorships, many are tapping direct fan support (subscriptions, tips), selling merch or digital products, and launching their own brands. More than 40% of social media users now tip creators (typically $5–$10) – a huge jump from just 17% in 2021. In a recent survey, 58% of online users said they’d pay for a creator’s content via monthly subscription and 63% had already tipped a creator at least once. This points to a cultural shift: audiences are growing more willing to financially support their favorite creators directly.

Platform Dynamics – Creators remain highly dependent on big platforms, but that relationship is evolving. TikTok and YouTube have emerged as the top platforms creators favor and earn the most from, each cited by 26% of creators as their #1 income source in 2023. YouTube’s established Partner Program (sharing ad revenue) paid out over $16 billion to creators in 2022 alone, while TikTok’s explosive growth offers unrivaled reach (over 1 billion users globally) – though its monetization programs have been more limited, pushing TikTokers to rely on brand deals and sponsorships. With intense competition and algorithm changes, creators have learned not to “put all their eggs in one basket.” Many now adopt a multi-platform presence to maximize discoverability and stability. For example, a video creator might engage fans on YouTube, Instagram Reels, and TikTok simultaneously, while also maintaining a newsletter on Substack and a membership on Patreon. This diversification helps mitigate risk from any single platform’s policy or algorithm changes. It also reflects a short-form vs. long-form content battle: short viral videos have dominated recent years, but longer content like podcasts and live streams retain dedicated audiences. Creators are spreading into all these formats – often repurposing content across them – to grow and keep their fanbases.

Industry Sentiment – The overall mood in the creator industry is optimistic but clear-eyed. In surveys, nearly 9 in 10 creators expected to earn more in 2024 than the prior year, and venture investors continue to see opportunity (with roughly $800 million/year in VC funding going into creator-economy startups in recent years). At the same time, creators voice challenges around burnout, monetization shifts, and platform dependence. Burnout is a real concern as algorithms reward high output and consistent engagement – many creators struggle to sustain the constant production cadence. Platform algorithms and policies can feel like moving goalposts: changes in feed algorithms or demonetization rules can suddenly impact a creator’s income. Indeed, ad revenues have been volatile (YouTube ad payouts to some creators fell during early COVID by ~33%) and half of consumers now use ad-blockers, pushing creators to seek non-ad income streams. Brand sponsorships remain the top revenue source for 77% of creators, but brands are selective, and creators must maintain trust with their audience to secure these deals. On the positive side, seasoned creators are increasingly advocating for better platform monetization and transparency, and platforms have started responding with new features (e.g. YouTube’s fan funding tools, TikTok’s creator funds, Instagram’s creator marketplace). In summary, market sentiment recognizes the creator economy as a high-growth, mainstream industry – one that is empowering millions of individuals to earn from digital content, yet still maturing in how to ensure sustainable, equitable incomes for the long tail of creators.

2. Popular Platforms and Their Value Propositions

The creator landscape is defined by a mix of social media giants, niche community platforms, and specialized tools. Each serves a unique role for creators. Below is an overview of some of the most popular platforms worldwide and what they offer creators:

- YouTube – Video powerhouse for ad revenue sharing. As the world’s largest video platform (2+ billion users), YouTube offers creators a robust monetization system: advertising revenue share (55% to creators), memberships, Super Chat donations during live streams, and a newly launched Shorts ad revenue pool. Its discovery algorithm and searchability give content long shelf lives. Unique value for creators: YouTube is often the most financially rewarding for video creators – it paid out over $30B to creators from 2018–2021 and over $16B in 2022 alone via the Partner Program. The ability to build a loyal subscriber base and earn passive income from a content library makes YouTube akin to a career platform for full-time creators. It requires more production effort than some platforms, but successful YouTubers can turn their channels into multi-million-dollar businesses.

- TikTok (and Douyin) – Viral short-form video and cultural trends. TikTok’s 60-second (now up to 3 min) vertical videos and uncanny algorithm have made it the cradle of viral content. Even small creators can amass huge view counts through the “For You” feed’s recommendation engine. Unique value: unmatched reach and growth potential – TikTok’s global monthly active users exceeded 1 billion, skewing younger, and it’s set cultural trends worldwide. Creators praise TikTok for rapid audience building and high engagement rates. Monetization has come via the TikTok Creator Fund, tipping, live gifts, and e-commerce (TikTok Shopping), but payouts from the fund are relatively low (many creators report only a few dollars for thousands of views). Thus, most monetize TikTok indirectly through brand sponsorships or by redirecting fans to other platforms/products. In China, TikTok’s sister app Douyin showcases the platform’s further potential: Douyin is deeply integrated with e-commerce, enabling influencers to drive live commerce sales (part of a Chinese live-stream shopping market worth ~¥5 trillion in 2023). TikTok is now heading that direction globally, which could unlock new income for creators. In short, TikTok offers fame and virality first, and is gradually improving ways for creators to cash in on that fame.

- Instagram – Visual storytelling and influencer marketing. Instagram remains essential for creators in lifestyle, fashion, travel, beauty and more. With around 2 billion users, it’s a top platform for influencer marketing – brands frequently collaborate with Instagram creators for sponsored posts and campaigns. Unique value: a highly visual medium (photos, short videos/Reels, Stories) that’s ideal for building a personal brand and aspirational content. Instagram gives creators multiple content formats (grid posts, Stories, IGTV/long-form, Reels, Lives) to engage followers. While direct monetization from Instagram is limited (the platform has experimented with bonuses for Reels views, a creator marketplace, and a paid subscriptions feature for exclusive content), the real financial draw is the access to brands and shoppers. Instagram’s integration of shopping tags and brand partnership tools helps creators earn via product promotion and affiliate marketing. In essence, Instagram is the showroom for creators – excelling at audience engagement and brand partnerships – even if it doesn’t cut creators an ad-revenue check like YouTube. Its parent Meta has been rolling out more creator features (like a paid verification program for increased reach and support, and linking with Facebook’s monetization programs), signaling that Instagram is doubling down on creators as key content drivers.

- Patreon – Membership platform for fan subscriptions. Patreon pioneered the direct subscription model, allowing fans (“patrons”) to pay creators monthly for exclusive content or perks. Unique value: reliable, recurring income independent of algorithms. Creators of all types – YouTubers, podcasters, artists, writers – use Patreon to offer paying supporters bonus episodes, early access, behind-the-scenes content, or community access. This flips the monetization model from advertiser-supported to fan-supported. As of mid-2024, over 273,000 creators have at least one paying patron on Patreon, up ~20% from two years prior. The platform’s popularity has led to impressive payouts: Patreon processed an estimated $4.1B in creator payouts in 2023, up from $2.8B in 2022. For mid-tier creators in particular, Patreon can far exceed their ad or sponsorship earnings by leveraging a small fraction of superfans. The trade-off is that creators must constantly provide value to subscribers to retain them, essentially running a small subscription business. Patreon’s success has inspired many competitors and alternative models (from YouTube’s Channel Memberships to Twitch Subs), but it remains the go-to for independent content monetization across fan communities.

- Substack – Newsletter publishing and paid content for writers. Substack burst onto the scene as part of a “newsletter renaissance,” enabling journalists, authors, and experts to monetize email newsletters. Unique value: it gives individual writers the infrastructure to run their own subscription publication with minimal overhead. Writers can send free and paid newsletters, and Substack handles billing and distribution in exchange for a ~10% fee. This has empowered many creators to leave traditional media jobs and earn directly from readers. By early 2023 Substack had over 2 million paid subscriptions on the platform (double the number from late 2021). Top Substack authors are making significant income – more than 50 Substack newsletters earn over $500,000 per year each, double the number of such high-earners from two years before. In fact, Substack revealed that its top 10 publishers collectively pull in about $40 million annually in subscriber revenue. For example, independent tech journalist Eric Newcomer grew his newsletter to 2,000+ paying subscribers (among 75k free readers) at ~$200/year, allowing him to surpass $1M in annual revenue in 2023. Such cases illustrate Substack’s appeal: it offers an alternative to ad-driven writing, rewarding niche, high-quality content with loyal readers. The model does require writers to continuously attract and retain subscribers, and competition is rising (e.g. traditional media launching their own newsletters, Twitter’s “Notes”/Subscriptions, etc.), but Substack has proven that the written word can be a thriving part of the creator economy.

- OnlyFans – Fan-paid content with an 18+ friendly reputation. OnlyFans is best known for adult content, but it’s also used by fitness coaches, musicians, chefs and other creators to sell premium content directly to fans. Creators can charge monthly subscriptions and/or one-off payments (for locked photos, videos, live sessions, etc.), and fans can tip or pay for custom requests. Unique value: an extremely lucrative payout model – creators keep 80% of earnings (OnlyFans takes 20%), one of the highest revenue shares in the industry. This high payout, combined with the freedom to post adult-oriented material not welcome on other platforms, attracted over 3 million content creators to OnlyFans and tens of millions of paying subscribers in the past few years. The platform’s growth during the pandemic was explosive: in 2023 fans spent $6.3B on OnlyFans (subscriptions + single purchases), yielding $5.3B paid to creators. Notably, one-time purchases (pay-per-view messages or clips) now account for ~60% of creators’ earnings on OnlyFans, outpacing subscriptions. This shows how creators can maximize revenue by selling personal interactions or exclusive drops. OnlyFans essentially proved the viability of the direct paywall model at scale – albeit turbocharged by adult content demand. Its success has led some mainstream platforms to explore similar models (e.g. Patreon and YouTube adding options to sell one-off digital goods). For creators, OnlyFans offers unparalleled monetization if they have highly devoted fans, though it comes with stigma and privacy considerations given its brand image. It remains a unique pillar of the creator economy focused on fan-driven income.

- Twitch – Live streaming and real-time community building. Twitch is the leading platform for live content, particularly gaming, but also “Just Chatting,” music, art, and more. It averages millions of concurrent viewers and 24+ billion hours watched annually. Unique value: real-time interactivity and a strong community culture. Creators (streamers) on Twitch broadcast live, often for hours, and interact with viewers via chat in real time – fostering a deep sense of connection. Monetization comes primarily from viewer subscriptions (fans pay $5/month to subscribe to a streamer’s channel, often to get perks and show support), donations/tips (via “Bits” or external services), and advertising. Top streamers also land sponsorships, but even mid-sized streamers can earn a steady living from many small fan payments. Twitch’s built-in tools like Twitch Prime (free sub with Amazon Prime), and raids/hosting (creators sending viewers to each other) encourage a supportive ecosystem. However, Twitch takes a 50% cut of subscriptions by default (some top partners get 70%), which is a bigger platform cut than YouTube or OnlyFans. In 2022–2023, Twitch faced criticism for this revenue split and for policy changes (e.g. limiting exclusivity and introducing new ad incentive programs), prompting some streamers to explore alternatives like YouTube Live or Facebook Gaming. New competitors such as Kick (launched 2023 with a 95% creator revenue share to entice streamers) are also emerging. Despite these challenges, Twitch remains the hub of live-stream culture in the West. Its unique selling point is that dedicated viewers on Twitch behave less like a passive audience and more like a fan club – they participate, chat, and financially support creators at rates other platforms envy. For creators whose content shines live (gaming, talk shows, tutorials, etc.), Twitch offers community engagement and monetization that’s hard to replicate elsewhere, albeit with some recent pressure to evolve its business terms.

- Linktree – “Link in bio” aggregator and traffic router. Unlike the others, Linktree is not a content hosting platform but a utility used by creators across all social networks. It provides a simple personal landing page where creators list multiple links (to their YouTube, Instagram, store, newsletter, etc.), solving the problem of social profiles allowing only one hyperlink. Unique value: Linktree became an essential tool for multi-platform creators to unify their online presence and drive followers to revenue-generating channels. It’s essentially a lightweight personal website. As of 2023, Linktree reported over 40 million users globally, reflecting its ubiquity in the creator community. The company has expanded its features – creators can collect tips through Linktree, embed videos, mailing list signups, and commerce links. According to Linktree’s data, the average top creator’s Linktree gets traffic from 12 different sources, underscoring how fans come from various platforms and how a single hub benefits creators. Notably, Linktree’s 2023 creator report highlighted a shift in where those links lead: while TikTok and YouTube remain the most-linked destinations, there was a 157% YoY increase in Linktree traffic going to Substack and a 33% increase to Patreon. This suggests creators are increasingly funneling followers toward deeper community or monetization channels (like newsletters and memberships) rather than just mainstream social profiles. In short, Linktree’s value prop is being the connective tissue of a creator’s digital ecosystem – it doesn’t provide audience or monetization by itself, but it maximizes the chances that a hard-won follower from Platform A discovers the creator’s work (or paid offerings) on Platform B, C, and D.

Other notable platforms: Facebook (including Facebook Gaming) has a large user base and introduced monetization like in-stream ads and fan subscriptions, though it’s generally secondary to Instagram/YouTube for creators. Twitter/X launched paid “Super Follows” and subscriptions to help writers and influencers monetize, but uptake has been limited so far. Podcast platforms like Spotify and Apple now enable paid subscriptions too, reflecting the trend of direct fan support across mediums. Additionally, regional platforms play key roles: for example, China’s Bilibili (for long-form video and anime/gaming content) and Weibo/WeChat for microblog and gated content, or India’s Moj and ShareChat which gained creator communities after TikTok’s ban there. The creator economy is truly global – but regardless of platform, creators gravitate to those that offer audience scale, monetization tools, and creative freedom. Each platform above has carved out a particular niche in that ecosystem.

3. AI’s Growing Influence on the Creator Economy

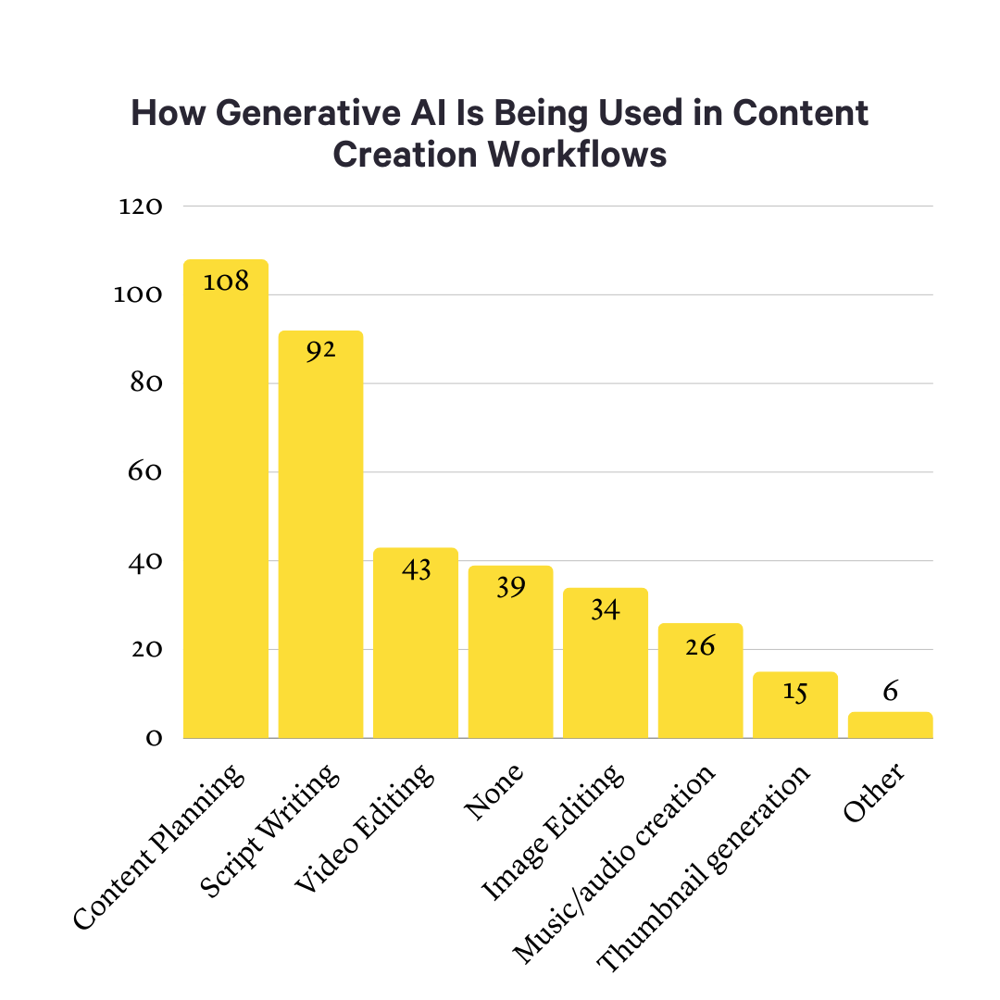

Artificial Intelligence has become a game-changer in how content is created, distributed, and monetized. Over the last two years, creators have rapidly adopted AI tools to enhance productivity and open new creative possibilities. In a recent late-2024 survey of creators, over 80% reported using generative AI in their content workflow in some form. Creators are leveraging AI at various stages: from brainstorming ideas to editing final outputs. The most common uses are content planning (using AI to research or outline topics) and script writing, with 57% and 48% of creators (respectively) saying they use AI tools for these tasks. Text-generation assistants like ChatGPT have become the go-to “creative assistant” for many, helping draft video scripts, blog posts or catchy captions in a fraction of the time.

How creators are using generative AI tools, based on a 2024 survey. Planning and writing are the top uses, followed by video editing assistance. Notably, only ~20% of creators said they do not use any AI in their process.

Beyond writing help, AI is making inroads in media production. Tools like DALL-E and Midjourney are enabling creators to generate custom images or graphics on demand (used by ~18% of creators in the survey), which is especially useful for those who need affordable visuals (e.g. indie game designers or bloggers who can’t hire illustrators for every post). AI-powered video editors (such as Descript, which can automatically cut silences or even synthesize voice) and mobile apps like CapCut are streamlining editing work (about 23% reported using AI for video editing tasks). For audio, AI can isolate and enhance voice tracks, or even clone a creator’s voice to dub content into other languages – something major YouTubers have begun doing to reach global audiences. Platforms themselves are integrating these capabilities: e.g. YouTube is piloting an AI dubbing service to translate creators’ videos, and TikTok offers AI filters and effects that creators use to spice up clips.

AI is also changing audience engagement and moderation. With large fan communities, some creators deploy AI chatbots to answer common fan questions or moderate comments/chat for toxicity (keeping the community civil without needing an army of human mods). Recommendation algorithms – a more hidden form of AI – have long shaped which creators get exposure. TikTok’s entire rise is credited to its AI-driven feed that surfaces the most engaging content to each user, allowing unknown creators to blow up overnight. This has pushed creators to analyze and adapt to algorithmic preferences (a sort of AI-oriented content optimization), e.g. structuring videos to immediately grab attention knowing the AI values early viewer retention. On the flip side, creators are wary of algorithm changes (often AI-driven) that can unpredictably alter their reach.

Importantly, AI is spawning new forms of creative content and even creators. We’re seeing the rise of virtual influencers – digitally-generated characters powered by AI that attract real followers. For instance, Lil Miquela (a virtual Instagram influencer) was an early example; more recently virtual streamers and AI VTubers have appeared, engaging fans without a human ever appearing on camera. Some human creators are experimenting with AI avatars of themselves: using programs to generate a talking digital “clone” that can present content 24/7. However, adoption of full AI avatars is still nascent – about 30% of creators said they are not at all interested in AI avatars for their brand, while a smaller segment (~23%) are very interested and exploring the idea. So there’s intrigue, but also caution, as authenticity remains a currency with audiences. Creators don’t want to alienate fans by appearing to hand off too much work to robots. In fact, that same survey found mixed opinions on AI’s impact: many creators loved the efficiency gains (some incorporating AI into daily work), while others reported no time saved or even extra effort, showing a learning curve on how to integrate AI effectively.

From a monetization perspective, AI is starting to play a role in analyzing and optimizing revenue. For example, AI analytics can predict which topics or products will resonate most with a creator’s audience, guiding smarter choices about sponsorships or merch. AI is being used to match creators with brands more efficiently too – influencer marketing platforms use machine learning to sift through millions of posts to identify good brand fits, opening more sponsorship opportunities even for micro-influencers. On the audience side, AI personalization means fans might soon get highly tailored content recommendations or even personalized messages from creators (using AI to generate one-to-one style communications at scale).

Crucially, the influence of AI extends to brands and advertisers in the creator economy. A 2023 Deloitte study found 94% of brands working with creators plan to use generative AI in their influencer marketing strategies – for instance, to quickly generate variations of creative briefs or even to create synthetic content featuring the creator (with permission). This could lead to scenarios where a creator’s likeness is reproduced by AI for an ad, allowing them to “be in many places at once” – raising new questions about licensing one’s AI avatar and revenue sharing.

Overall, AI’s impact on the creator economy in 2023-2024 has been largely empowering: automating drudgery (editing, transcriptions), amplifying creativity (providing endless ideas and effects), and enabling scalability (one person can now do the work of a small team with AI helpers). But it also introduces challenges around authenticity, originality, and fairness. As AI-generated content proliferates, standing out will require creators to put even more of their personal human touch and brand into their work. We’re likely to see a hybrid creator model going forward – where the most successful creators leverage AI for efficiency and experimentation, but double down on the human elements (personality, live interaction, personal storytelling) that forge genuine audience connections.

4. Emerging Business Opportunities in the Creator Economy

With the creator economy’s robust growth and ongoing transformation, a wide array of opportunities has opened up for entrepreneurs and investors to build new services, platforms, and monetization models. Here are several key opportunity areas, backed by recent trends:

New Monetization Models: The evolving ways fans spend on creators signal opportunities for innovation. The success of platforms like OnlyFans (with one-off content purchases) and Patreon (subscriptions) shows that fans are willing to pay for content in different structures beyond traditional ads. We’re seeing a rise in digital products and experiences sold by creators – from exclusive videos, PDFs, and filters to paid community access and virtual events. In 2023, OnlyFans saw single-purchase content (pay-per-view posts, messages) grow 70% and account for nearly 60% of creator revenue. Now mainstream platforms are catching on: YouTube and Instagram have introduced features for creators to sell digital goods and gated content. Startups can capitalize on this by building specialized marketplaces or tools for creator commerce. For example, services that help creators easily package and sell bite-sized digital products (tutorial files, printables, filters, music snippets, etc.) could thrive. Similarly, facilitating paid fan experiences – one-on-one video shoutouts, small-group workshops, virtual meet-and-greets – is a growing niche (seen in apps like Cameo or Looped). The fact that more than half of consumers say they’d pay $1–$15 monthly for a favorite creator’s exclusive content underlines that there is still untapped demand. Entrepreneurial opportunity lies in making it seamless for creators to monetize that demand, whether via better payment integration on existing socials or new platforms built around specific content verticals (e.g. a platform just for fitness creators to offer paid classes).

Creator Tools and Services (the “B2B” side of the Creator Economy): As the number of creators has exploded, so has the need for infrastructure to support them. This is a rich area for startups – essentially providing the picks and shovels to this gold rush. One obvious space is AI-powered creator tools (as discussed above): from editing suites to thumbnail generators to AI co-writers. Investors have been actively funding such tools in the past two years, betting that creators will pay for anything that gives them a competitive edge or saves time. Another area is analytics and multi-platform management. A creator active on 5 platforms needs insights into which content performs best where, the demographics of their fanbase, and how to grow strategically. Tools that centralize analytics across YouTube, TikTok, Instagram, etc., or that allow scheduling and repurposing content in one dashboard, are in high demand for efficiency. We also see opportunity in community management software – for example, Discord became a favored way to run fan communities, and now Discord itself allows creators to set up paid subscriber-only channels. Startups that help moderate communities, integrate them with content drops, or gamify fan engagement can ride this trend of creators seeking to own their audience relationship off the big social platforms.

One burgeoning niche is creator fintech: treating creators as a distinct customer class for financial services. Creators often have irregular income streams (dependent on virality or seasonal ads) and global fan payments, which legacy banking doesn’t serve well. Companies like Karat (which offers credit cards and banking designed for creators) and Stir (tools for splitting revenue among collaborators) have made headway. There’s room for more innovation in helping creators with taxes, royalties, and revenue smoothing (e.g. offering advances or loans against future earnings – a model pioneered by Spotter which pays YouTubers upfront lump sums in exchange for their future ad revenue). Given the billions in payouts flowing through the ecosystem, fintech solutions for faster, more flexible access to that money will attract investors.

Emerging Niches and Content Verticals: The creator economy is diversifying into every imaginable interest area, which means opportunities to build specialized platforms at the intersection of content and other industries. For instance, education is a promising frontier – creators who are subject-matter experts (from coding to cooking to language learning) are monetizing through online courses, cohort-based classes, or subscription learning communities. Platforms like Teachable and Kajabi have grown by catering to these edu-creators, and demand for live tutoring or mentorship marketplaces is rising. Another niche is the B2B/professional content creator – e.g. LinkedIn influencers, or experts creating premium content for business audiences. Services that help package and monetize professional knowledge (perhaps through subscription reports, paid Slack groups, or webinar series) can tap into corporate budgets and high willingness-to-pay from professionals seeking insights.

Geographic and Demographic Market Gaps: There are significant opportunities in adapting the creator economy model to different regions and audiences. In markets like India, Latin America, and Africa, huge user populations are coming online and embracing social platforms, but monetization infrastructure lags behind the US/Europe. For example, India’s creator economy was valued under $1B in 2023 but is forecast to grow fourfold by 2030, suggesting a ripe environment for local platforms and tools. Startups that localize features like tipping, or enable easier cross-language monetization (imagine a tool that auto-translates and dubs an American creator’s videos for Spanish or Hindi audiences) can unlock new revenue streams. Even within mature markets, demographics like Gen Z versus Gen X/Boomers present different needs. Interestingly, the share of older generations among creators is growing (from 27% in 2022 to 35% in 2023 for Boomers/Gen X). This could spur opportunities for platforms oriented toward older creators and audiences – for instance, sites for retired professionals to share expertise or hobby content (with appropriate UI and community norms). Likewise, kid-friendly creator platforms (beyond YouTube Kids) could emerge, or platforms addressing parents who want safer environments for young influencers.

Live Commerce and Social Commerce: Inspired by China’s $700+ billion live-stream shopping industry, Western markets are trying to crack the code on blending content and commerce. There is a massive opportunity for those who figure out how to make live selling work outside China. TikTok is integrating shops; YouTube added a shopping tab and live product tags; startups like Whatnot and Popshop are focusing on collectibles and niche live auctions. An entrepreneur might focus on specific categories – say a live-stream platform just for fashion and beauty creators to host trunk-show-style streams – or on technology that makes any stream shoppable (AR try-ons, one-click purchasing in streams). With 15 million+ professional livestreamers in China (1 in 100 Chinese citizens!) engaged in selling, it’s clear this model can also create jobs at scale. We can expect investors to continue backing efforts to replicate that success globally. The key will be tailoring it to local culture and finding the right incentives for creators to participate (e.g. higher commissions, or combining entertainment with commerce in a way that doesn’t feel too salesy for Western viewers).

Creator-led Brands and IP: Some of the biggest successes in the creator economy come when creators transcend content to launch products and businesses. We’ve seen YouTube and TikTok stars create makeup lines, snacks, fitness apps, merchandise empires, even restaurants (e.g. MrBeast Burger’s virtual fast food brand). These creator-led brands leverage a built-in fan customer base and can achieve impressive sales – for example, influencer Logan Paul’s sports drink “Prime” reportedly sold hundreds of millions of dollars in its first year, leveraging his and KSI’s fan followings. This trend opens opportunities for investors to partner with creators as brand builders. Traditional venture capital might back a creator’s startup (as in the case of celebrity creators launching tech platforms or consumer product lines) – essentially treating popular creators as the next generation of media companies or franchises. We are also seeing the rise of agencies and incubators that specialize in spinning up creator brands, which need investment, supply chain, and marketing support. Another angle is licensing and IP development: turning a hit YouTube kids’ show or a podcast into a Netflix series, book, or toy line. Creators increasingly own valuable intellectual property, and studios are hungry for proven content – so acting as a bridge (or funding vehicle) for that adaptation is an opportunity.

Web3 and Decentralized Creator Platforms: While the cryptocurrency/NFT boom of 2021 has cooled, the underlying idea of decentralized creator ownership still presents an innovative area. During the boom, some creators launched NFTs or social tokens to monetize their work and build mini economies with their fans. The concept of fans having a stake in a creator’s success (e.g. holding a token that grows in value as the creator’s popularity rises) is experimental but game-changing. Startups in the Web3 creator economy realm are exploring ways to give creators more ownership and direct monetization without platform middlemen – for instance, decentralized video hosting where creators earn crypto based on viewing, or NFTs that grant access to exclusive content or community roles. While mainstream adoption is currently low (many fans aren’t crypto-savvy, and there were trust issues after some scams), the long-term potential of blockchain in creator monetization could resurge. Investors with a higher risk appetite may find opportunities in building the infrastructure for digital ownership and trading of creative works, which could become more normalized in the future (for example, a music artist selling NFT-based royalty shares of a song to fans).

In summary, the creator economy’s rapid growth has created a vibrant ecosystem of startups and investment prospects. The past two years have demonstrated that creators are not just a marketing channel but a new economic force – one that demands dedicated tools, platforms, and services. Whether it’s enabling a teacher in Nigeria to monetize a global YouTube following, helping a gamer in Los Angeles turn streaming into a full-time job with financial stability, or building the “Shopify for creators” to launch their own product lines, the opportunities span industries and geographies. The creator economy is still in an early chapter of its story. Entrepreneurs and investors who understand the needs of creators – for monetization diversity, ownership, efficiency, community engagement, and authenticity – will be best positioned to ride the next wave of innovation in this space. As one industry expert put it, creators have proven they can “spark cultural movements” and even shape consumer behavior; enabling those creators to thrive is now a business opportunity with virtually global scale.